THE OLD joke runs that if you ask two economists a question you will get at least three answers. That wasn’t the case at a Growth Commission conference on ‘Mending Britain’s Broken Economy’ at the University of Buckingham. The unanimous view of the many eminent economists there (who included TCW writer Ewen Stewart) was that the UK’s economy is stuffed (industry term). There is no way the current economic trajectory can succeed, as illustrated below.

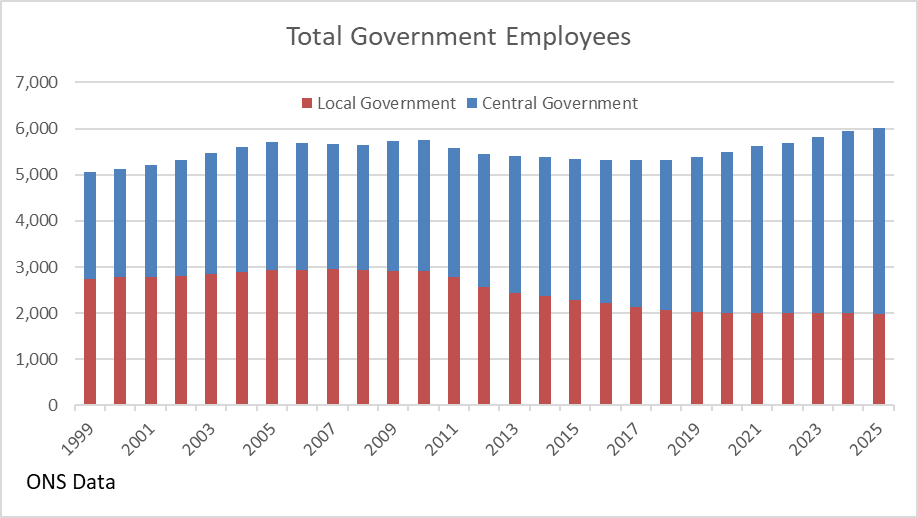

In last quarter-century the state’s employee headcount has increased by 20 per cent. That, of course, means an increased demand on the public purse (your taxes) to cover the payroll and the pensions. In 1999 government spending was 35 per cent of GDP; today it is 46 per cent. That spending comes from taxation or government borrowing. Successive governments have increased both. Of the £14billion of government debt issued last month, a staggering £13billion was spent on debt interest.

The government is taking more money and employing more people to deliver less stuff. The tax take has increased to the point of being a brake on the economy. Rachel Reeves’s policies have triggered capital flight and a worker exodus. The UK’s lamentable growth is amongst the lowest in G20 and G7. Were the UK a company it would have called in an administrator long ago.

The economists at the conference saw three routes out of the UK’s debt hole. Good luck, which they rated a 10 per cent probability, runaway inflation (50 per cent) or some financial crisis triggering default or an International Monetary Fund (IMF) intervention. They noted that the IMF lacks the funds to bail the UK out.

The solution to the problem is for the UK to start growing its economy. Rachel Reeves purports to understand this. But delivering growth requires investment capital and bank finance, above all for the UK’s small and medium enterprises (SMEs) which provide some 60 per cent of employment and 50 per cent of private sector turnover in the UK. And less regulation.

Unfortunately, as the speakers revealed, SMEs are being starved of capital in general and bank lending in particular. Since the 2008 financial crisis, UK bank lending to SMEs has fallen from 2 per cent of GDP to about 0.5 per cent. At the same time the banks’ holdings of UK gilts have risen massively and unhealthily.

Over-regulation was one of the key reasons cited for the poor performance of the UK. One American banking expert, Professor Jill Cetina, suggested that the UK needed more smaller banks rather than a few monoliths too big to be allowed to fail, plus a handful of challenger banks. She pointed out that Texas has many small banks (termed ‘community banks’) which are fundamental to the Texan oil-boom economy. Small banks can be allowed to fail as there is no risk of systemic collapse.

The new banking regulations won’t, can’t, remove emerging systemic risks. Worse, regulation protects market incumbents who can afford lobbyists and PR machines to maintain the status quo and stifle competition.

Make no mistake, the UK’s dire economic situation stems from a consistent lack of growth. That in turn comes from denying the engine room of the economy access to capital, a consequence of ill-considered regulations, for which the responsibility ultimately lies with Parliament. As most modern careerist politicians have little experience of finance (or much else for that matter), they rely heavily upon their civil servants for briefing on the decisions they must make.

Unfortunately those civil servants almost invariably lack experience of banking or the commercial world as they too are careerists – there is very little churn of non-civil servants into top jobs. While various quangos that run our lives, including the City of London and the finance industry, their masters remain in the Treasury. Despite the evidence, the civil service and the whole public sector believe in prescriptive regulation. (So of course does most of Westminster, politicians exist to pass laws and laws become regulations).

The economic orthodoxy has become one of seeking a managed economy, with a large state machine, concomitantly high taxes, low growth and ever more regulation. The conference was pretty much unanimous that this means the UK is in a self-inflicted death spiral. The actions required to change the UK’s trajectory are straightforward, a smaller state (requiring less tax) and a balanced budget (meaning no more borrowing). The last person to attempt this trajectory change in the UK was Liz Truss.

She gave a frank and forthright presentation on the dysfunctional split of the UK economy’s managers: the Bank of England, the Treasury and the Office of Budgetary Responsibility (OBR). They operate in splendid isolation from each other. Thus on the eve of the Truss mini-Budget the Bank blithely announced a £40billion quantitative tightening (QT) programme without first notifying the Treasury. QT is generally loss-making, so the Bank’s actions would have needed cash from the Treasury, who knew nothing of it. It also transpired that the Bank was aware of the Liability-Driven Investment (LDI) problem but had not deigned to share that information with the Treasury. (The LDI scheme got itself into a doom loop when the bond markets started to adjust to the new budget. That doom loop triggered forced sales of UK bonds, which the bank had to hoover up while the bond yield soared.) While the Bank is independent of the Treasury and Westminster, it’s exceptionally strange that it didn’t consider the implications and timings of its actions.

The Bank is independent. There was some disagreement between the assembled economists as to whether this was true, was a good thing or was fixable. After so much agreement, watching veteran economists going at each other hammer and tongs was entertaining. There was no consensus on whether changing the management structure of the Bank or giving it more or less autonomy would fix the UK’s economic problems.

That those problems derive from an incompetent, unaffordable large state is self-evident to anyone who can count. Reducing the size of the state is, unfortunately, politically difficult – not least because the ‘progressives’ (as some socialists now style themselves) have captured the vocabulary. Any attempt to cut the wasteful state is trumpeted as ‘austerity’, which is treated as a synonym of inhumane.

Worse, progressivism is embedded in British universities, with some 60 per cent to 80 per cent of staff ‘left wing’ or progressive. The general population is thought to be about 10 per cent progressive activist. As the civil service and large companies recruit graduates, it seems inevitable that the progressive agenda, already deeply embedded in industry, media and government, will become the majority view in the key organs of the economy, but not the population.

Whether the economically literate parties (those of the right) can win power in such an environment is an open question. Whether they could then force through the necessary changes is equally unknown.

The certainty is that if they don’t the UK’s future is bleak.

A longer version of this article appears on Views From My Cab and is republished by kind permission.