IT IS a common and enduring claim that Margaret Thatcher’s government ‘sold off’ or privatised the UK’s oil, gas, and energy assets during the 1980s. Variations of this claim have been repeated on social media and in TV and radio interviews since the outbreak of conflict in the Persian Gulf. It is wrong on many levels.

Firstly, neither Thatcher nor any other government ‘sold off’ the country’s oil and gas resources. In 2002, the Labour government under Tony Blair abolished royalties on the volume of oil and gas extracted and replaced them with taxes on profits. The government also issues and charges for licences to explore and develop the territorial waters and continental shelf for oil and gas, as well as build pipelines to the coast, etc.

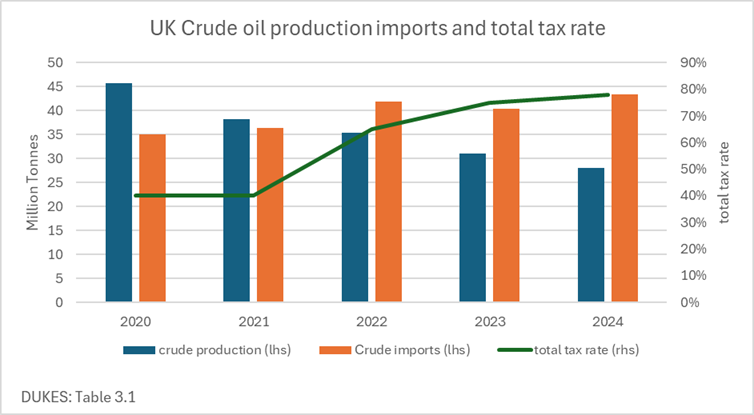

The UK certainly does not knowingly give away the oil and gas, either. The taxes on oil and gas company profits are more than three times those of other companies, and oil and gas firms have fewer allowances. Should a company be lucky enough to find oil and/or gas, they have to pay a ring-fenced corporation tax of 30 per cent and an additional supplementary charge of 10 per cent and finally a windfall tax (the Energy Profits Levy) of 38 per cent, taking their total tax rate to 78 per cent.

The details of these taxes come from my paper for the Great British Business Council, entitled Premeditated Industrial Destruction? How the UK destroyed its industry and a plan to reverse this. It says:

Ring-fenced corporation tax (RFCT) of 30 per cent

These taxes are charged on ring-fenced profits from oil and gas produced in the UK and the UK Continental Shelf. Ring-fenced profits are those that cannot be reduced by losses from other parts of the company. This 30 per cent tax rate was intended to ensure the UK government received a fair share of returns from the UK’s natural resources. The standard UK corporate tax rate is currently 25per cent.

The Supplementary Charge (SC) of 10per cent

The 10 per cent Supplementary Charge was introduced in 2016 and is also applied to ring-fenced profits, but without a deduction for financing costs. However, the SC permits deductions for the Investment Allowances, Cluster Area Allowance, and Onshore Allowances. The Cluster Area allowance was introduced in the Finance Act 2015 and provides a 62.5 per cent deduction on qualifying expenditure incurred in a designated cluster area. So far, there is only one cluster area: the Culzean Cluster Area in the North Sea. The Onshore Allowance was introduced in the Finance Act 2014 to support the development of onshore oil and gas projects and allows 75 per cent of capital expenditure to be deducted. The Investment Allowance is currently 62.5 per cent of investment expenditure.

Energy Profits Levy (Windfall Tax)

Introduced following the Russian invasion of Ukraine as a temporary tax on the ‘windfall profits’ of oil and gas companies. Originally set at 25 per cent for three years, the EPL has been increased and extended twice and is now 38 per cent through to 2030. The 29 per cent investment allowance has been removed, and the decarbonisation investment allowance has been reduced to 66 per cent. After its expiry in 2030, the windfall tax will be replaced by a permanent tax. The EPL will expire before 2030 if the six-month average price for both oil and gas is at or below the Energy Security Investment Mechanism threshold of £71.40 per barrel of oil and £0.54 per therm for gas.

The Government also charges offshore licence holders an Oil and Gas Levy, whether the licence is in production or in pre-production. This is paid annually to the North Sea Transition Authority (NSTA). It also charges fees for pipeline authorisations, offshore gas storage licences, CO2 storage licences, and pollution prevention and control. The NSTA also charges fees for licence applications, drilling consents, pipeline works, consent to extend a licence, or to amend a work programme approval.

The Government now takes more money from North Sea oil and gas profits than the companies that do all the work and make major investments in exploration, plant, and equipment. Or at least it used to. Now, with tax rates so high and restrictions on new wells so tight, most companies operating on the UK side of the North Sea are closing down or reducing their production, while UK crude imports are increasing.

The OBR’s March estimate of revenues from all three oil and gas taxes mentioned above was estimated at only £200million in 2028/9 and expected to drop to just £100million in 2029/30.

In 2022/3, the Government raised £9.9billion in oil and gas tax revenues. The 25 per cent windfall tax was introduced at the end of May 2022 and was due to expire at the end of 2025. Instead, justsix months later, the tax was increased to 35 per cent and extended until the end of March 2028. In November 2024, it was increased to 38 per cent and extended to 2030. Consequently, revenue collected fell from £9.3billion in 2022/23 to £5.5billion in 2023/24 to £4.4billion in 2024/25, and the OBR expects the 2025/26 oil and gas tax revenues to drop to £2.7billion.

To put that into perspective: Norway collected NOK373.1billion in oil and gas taxes in 2025, equivalent to around £28.8billion, while the UK raised just £4.4billion in 2024/5 despite owning a much greater proportion of the North Sea fields. If we include Norway’s States Direct Financial Interest (SDFI) income, environment fees, and Equinor dividends, the total net Norwegian government petroleum cash flow in 2025 was NOK655.8billion (£50.7billion). Why the disparity? Norway encourages more production and invests in that production, so it makes more money from it.

This is nonsense for North Sea gas. The UK does not have the facilities to convert natural gas to a liquid and transport it to countries not connected by pipeline. Converting gas to LNG requires specialist equipment and is a very expensive process, so it is only financially viable if the natural gas is relatively cheap to start with. Unless the UK increases its gas production as dramatically as the US did after its shale gas revolution, thus lowering US natural gas prices by a quarter, it is unlikely that the UK will ever be a commercially viable place to spend about $6billion to build an LNG plant, as Norway and Russia have done. Building an LNG plant in the UK would have been an exceptionally risky investment under the current and previous governments, who did and are doing everything possible to discourage UK oil and gas production.

But what about oil? It can be easily transported. North Sea crude is sold on the open market and typically goes to UK, Dutch, German and Scandinavian refineries. Refineries purchase different grades of oil based on price, availability, transport cost, product demand, and their refinery configuration (as discussed here). But that doesn’t mean that once the crude oil reaches a refinery, the UK market will never see it again. The UK remains a major buyer of European refined oil products, especially diesel. Two of Europe’s largest refineries are in Rotterdam: one is owned by Shell and the other by BP. Neither company has a refinery in the UK. This is why UK trade with the Netherlands appears disproportionately high, given their population sizes: we export crude oil to them and then import refined products, such as diesel, back.

The UK now has only four refineries, all of which have deep water ports and import various grades of crude from international oil fields. It is strange that so many commentators seem to think that the UK should restrict exports of its North Sea production but expect UK refineries to be able to import as many different grades of crude as they need from other countries.

The only European refinery that primarily used UK North Sea crude was the recently closed Grangemouth refinery because the forties pipeline system brings crude from dozens of North Sea fields to the Kinneil Terminal, which is part of the Grangemouth complex. Grangemouth also imported international crude oil via the Finnart Ocean Terminal, connected by a pipeline across Scotland.

North Sea crudes tend to be light, sweet crudes that are more suited to petrol, diesel, jet fuel, and naphtha production. The UK’s four refineries were all built mainly between 1950 and 1970, before the development of North Sea oil and when most UK vehicles ran on petrol. Now, diesel demand is higher, as car owners were encouraged to switch to diesel in the early 2000s to lower CO2 emissions, and larger trucks, machinery, and farm equipment are mainly diesel-powered. Most EU refineries are configured to produce more diesel, as there are more diesel cars on the continent, so demand for diesel is higher.

Exporting crude and importing refined products is no different from any other type of trade. For example, the UK exports milk to Ireland and imports butter and cheese, without activists complaining that there is no point milking any more cows once domestic demand has been satisfied. The fact that some North Sea oil will be exported is not a valid excuse for preventing companies from producing it; it may be exported, but so what? UK refineries also import other types of crude oil from other countries.

Before the war in the Persian Gulf, imported US LNG could be landed in the UK for about the same price as North Sea natural gas, so it is a mistake to suggest that the UK is importing ‘more expensive’ LNG. However, Norwegian gas and LNG imports impose a significant opportunity cost, as the UK economy misses out on tax revenues, high-paying regional jobs, and a lower trade deficit.

Environmentalists opposed to North Sea gas production should also note that LNG wastes a lot of energy. Using UK North Sea natural gas is better for the global environment, although it is counted as a UK UNFCCC emission. Natural gas requires less energy to produce and provides the UK with a secure supply of gas for domestic heating, electricity generation, industrial heat, and as an input for fertiliser and chemical production. Again, I quote from the GBBC paper:

‘Besides the obvious financial benefits of using natural gas from the North Sea: increased tax revenue, increased regional employment and an improved balance of payments, there is also an energy bonus. The highest Energy Return on Energy Invested (ERoEI) is achieved from a conventional gas field. The ERoEI is between 20:1 and 28:1. That means we get over 20 times as much energy out of a natural gas field as we put in to extract the gas. However, imported LNG has a dramatically lower ERoEI. The liquefaction process consumes about 10 per cent of the gas’s energy, and the shipping fuel and regasification further reduce the energy returned. Imported LNG has an ERoEI of less than 10:1. Importing LNG from the US only makes financial sense because fracking in the US has lowered the US gas prices so much that there is still a financial gain after converting it to LNG and transporting it across the Atlantic.’

Some media commentators, MPs and environmentalists seem to believe that Norway is like some developing or despotic countries with full state control of its oil and gas operations. That is not how the Norwegian system works. There are no besuited Norwegian public servants working on oil rigs in the North Sea. The Norwegian government, like almost all other countries, sells exploration and production licences to commercial oil and gas companies and then taxes their profits after allowing them to expense their exploration and development costs (unlike the UK).

Norway collected seven times as much in taxes from oil and gas companies in 2025, because it encourages oil and gas production, without including the income Norway receives from the SDFI, which holds direct stakes in more than 40 producing fields, accounting for about 30 per cent of Norway’s total oil and gas reserves. The SDFI does not automatically take a stake in all new fields; instead, new licences are awarded through competitive licensing rounds and awarded by the Ministry of Energy. Consequently, many licences are owned and operated entirely by private companies. There are 24 different oil and gas companies operating on the Norwegian continental shelf, including Aker BP, Var Energi, Shell, TotalEnergies, and ConocoPhillips.

Although Equinor started life as the state-owned Statoil, it never had exclusive rights over Norway’s oil and gas resources. Norway has always used a licensing system for companies operating in its waters, as almost all other countries do. Equinor was partially privatised in 2002 and listed on the Oslo and New York stock exchanges. The Norwegian government still owns two-thirds of Equinor’s shares and collects dividends as well as taxes. There was a law that Statoil had to own 50 per cent of all licences in Norwegian waters, but it was dropped by 1985. Equinor is now a commercial company and must bid for Norwegian licences along with other oil and gas companies. It also operates in 36 countries, including on the UK side of the North Sea.

It is hard to fathom how this got past the Financial Times’s eagle-eyed editors, but it did: ‘More than 65 leading UK scientists have warned against new oil and gas drilling in the North Sea, urging the Government instead to prioritise renewable energy as a more cost-effective response to the energy crisis.’

No amount of ‘renewable energy’ can replace jet-fuel, petrol, diesel, bunker fuel, or heating oils. Nor can renewable energy produce the industrial heat needed to produce cement, ceramics, glass, steel or aluminium. Nor can renewable energy replace the hydrocarbons needed to produce chemical feedstocks for plastics, fertilisers, and pharmaceuticals. Nor can renewable energy create bitumen for asphalt, carbon fibres, or armaments and ammunition. Yes, some products can be recycled, possibly using renewable energy, but we still need the original materials before they can be recycled. Even UK renewable electricity needs a backup plan, and this is also provided by gas. It is surprising that these ‘leading scientists’ don’t know this.

This article appeared in Catherine McBride’s substack on April 3, 2026, and is republished by kind permission.