My last post yesterday was kind of a quick, one-day-news-tour around the wreckage #Bidenomics has left strewn across the American landscape. To wit, the inflation pressures, employment pressures, and unending social reengineering pressures.

Being subject to the progressive grifting regime has not been beneficial in the least for the country’s psyche, soul, or security, either safety or financial.

One tidbit that dropped yesterday, which I only bumped up against, was the explosion of credit card delinquencies. In this Biden induced time of wage stagnation and job insecurity coupled with exploding household costs, it’s not really surprising when even formerly comfortable people are feeling the pinch.

…Also out today: Stress? What stress? #Bidenomics baby!

US credit-card delinquency rates were the highest on record in the fourth quarter, according to a Federal Reserve Bank of Philadelphia report.

Almost 3.5% of card balances were at least 30 days past due as of the end of December, the Philadelphia Fed said. That’s the highest figure in the data series going back to 2012, and up by about 30 basis points from the previous quarter. The share of debts that are 60 and 90 days late also climbed.

“Stress among cardholders was further underscored in payment behavior, as the share of accounts making minimum payments rose 34 basis points to a series high,” according to the report.

That’s signaling a struggle in the ranks right there. What did our geriatric, pudding-brained chief executive tout as relief for Americans bent over from carrying his loads?

Why, he’s knocking those late fees back to $8. How ’bout that, pardners?

They don’t call him “MBNA Joe” for nuthin’ – man’s bought and paid for by the card industry.

The Consumer Financial Protection Bureau’s new regulations will set a ceiling of $8 for most credit card late fees, or require banks to show why they should charge more than $8 for such a fee. The effort will save Americans up to $10 billion a year, the agency estimates.

The push comes a year after President Joe Biden vowed to ban junk fees in his 2023 State of the Union address, calling them “unfair.” Junk fees generate big money for businesses, ranging from airlines to financial services firms, with consumers paying at $90 billion annually in excessive charges, the White House said on Tuesday.

LET’S JUNK BRANDON

I’m sure every family who has to wonder if their payment hit and covered the interest enough to buy the next week’s gas and food is as thrilled and delighted.

There are a lot of those families out there right now, thanks to this risible economic team, and they are facing a mountain of challenges.

The nation’s mounting credit card debt threatens to swamp its savings.

More than one-third of American adults – 36% – have more credit card debt than emergency savings, according to an annual survey by Bankrate, the personal finance site. In more than a decade of polling, the figure has never been higher.

That is one of several recent reports that show consumers falling behind on their credit cards.

Roughly half of all credit card holders now carry balances from month to month, Bankrate found in another survey, up from 39% in 2021.

Households are struggling to pay bills, less mind add to their savings. Treading water wears you flat out if your feet never, ever seem like they’re going to touch ground.

…Credit card debt is rising at a time when America is struggling to save.

The personal savings ratestood at 3.8%in January, according to federal data, meaning that consumers set aside only a smidgen of their income as savings.

That’s not an all-time low, but it’s close. For most of the past 10 years, the savings rate has ranged above 5%.

Here’s another absolutely deadly comparison for #Bidenomics vs the Trump years, and, again, don’t think people won’t remember the fears back then.

Americans are saving at an unusually high level after Trump’s tax cuts

ZOMG PEOPLES HAVE TOO MUCH MONEYZ!!!

I thought saving was a good thing – financial security, stability. But no. The Trump tax cuts were only for the wealthy, remember?

Americans have been socking away an unusually high rate of their income since the Great Recession, which economists warn could become harmful to the economy over an extended period of time, according to the Wall Street Journal.

Why it matters: Economists think that if the saving rate surpasses investments for several years, it could hinder economic growth and make it difficult for the Federal Reserve to cut interest rates to boost growth during the next downturn.

Details: The personal-saving rate — or the percentage of income that people save after taxes — rose from 3.7% in 2007 to 6.5% in 2010, after the end of the Great Recession. This is standard and is usually followed by a decline as people grow more optimistic about the economy during an expansion and spend more.

However, the personal-saving rate continued to rise to an average of 8.2% in the first 7 months of 2019 — despite U.S. consumers experiencing historic levels of confidence in the economy.

In total, savings outpaced spending and investing in 2018

Not only were people saving their butts off during 2019, they were doing it in spite of a great economy, completely baffling the economic Experts™.

Things were so good that people had money to save on top of feeling that their lives were humming along just fine.

ZOMG NOES! SAVING BAD, ORANGE MAN BAD

Three years of Joe Biden, and we’re all safely back in the poorhouse, making room for more new arrivals every day. This is particularly true as interest rates on those cards are making it mighty hard to claw your way out.

…But the federal survey doesn’t fully capture the run-up in credit card rates, which began in mid-2022.

The average interest rate charged on credit cards rose to 21.5% in November 2023 from 15.1% in May 2022, according to WalletHub.

Card rates rose along with interest rates generally: Federal regulators launched a historic campaign of rate increases to tamp down inflation, which peaked at a 40-year high of over 9% in the summer of 2022.

The average credit card interest rate is 27.89%, according to Forbes Advisor’s weekly credit card rates report.

The Federal Reserve keeps tabs on the average interest rate that U.S. consumers pay for a variety of different financial products—credit cards included. In February 2024, the average credit card interest rate in the U.S. on accounts with balances that assessed interest was 22.63%, according to The Federal Reserve.

Up five percentage points in a shade over two months. Feeling used and abused yet?

…Let’s say you have a balance of $6,360, at an interest rate of 22%. If you make the minimum payments, it’ll take you about 25 years to retire the debt, and you’ll pay $11,000 in interest on top of the principal, according to a Bankrate calculator.

That’s at 22% – if you’ve missed payments, good luck with a rate that low.

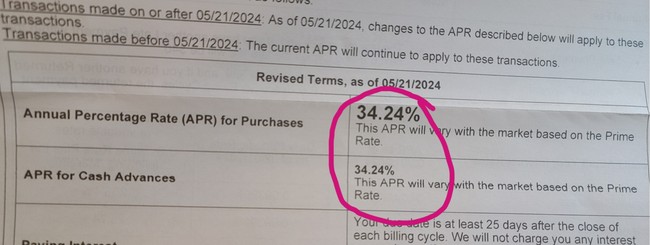

I got something in the mail today that kind of had me staggering a bit. Something I hadn’t even really given a second thought to because we’re blessed to be able to cover everything when bills hit. But one of those card term change disclosure forms came from our Shell gas card. Mind you, this is an account we’ve had with them for over thirty years, and use constantly since a station is convenient. We never carry a balance.

Now I’m thinking they’re pissed at us for it.

Because of last night’s post, I actually took more than a cursory look at the paperwork and damn near dropped it.

HOLY SMOKING EYEBALLS

That’s unconscionable. I can’t imagine if we had a family to support and, by necessity, had to carry a balance here or there – maybe everywhere, depending on the circumstances.

I can do that math. It would shortly eat you alive.

I review credit reports everyday. Folks are in Trouble!

The bank prime rate – which usually runs about 3 points higher than the Fed funds rate – is at 8.50% today. How that translates to a 35% interest rate on any card in good standing (never mind a decades-old account coupled with outstanding credit) is an abomination and flat-out highway robbery.

That this administration’s miserable handling of this country’s economy has allowed this tragedy – and it is going to be a full-blown disaster – to occur is a complete abrogation of their responsibility to the American people.

A callous and indifferent, “Oh, look! I got you $8!”…